Choosing a payment terminal is no longer just a banking formality. For a long time, the process was straightforward: you got a terminal from your bank, signed the contract, and started accepting payments. Today, the market has completely transformed. Alongside traditional banks, players like SumUp, Smile & Pay, PayPlug, myPOS, Flatpay, or Easytransac offer very different models—in terms of terminal pricing, fees, and commitments.

The problem? Comparing these offers can be a real headache. Behind an advertised rate of 1.29% or a terminal priced at €39, the actual cost can vary by as much as three times depending on your business. The cost of a payment terminal isn’t just the purchase price or a percentage per transaction.

The real question is: Which solution is actually the most cost-effective for your business in the long run?

Banks or fintech companies: two opposing philosophies

The banking model: long-term leasing

Traditional banks work with manufacturers such as Ingenico or Verifone. The POS terminal is rarely sold—it is leased as part of a contract tied to your merchant account. You can generally expect to pay between €20 and €60 per month, with a commitment period that often exceeds 24 months.

At first glance, it’s reassuring: a single point of contact, a familiar framework. But over 3 to 5 years, the cost adds up. At €40/month over 4 years, that’s nearly €2,000 in fees, not counting commissions. And these commissions, presented as “competitive,” actually vary depending on the card type (CB, Visa, Mastercard, Amex, premium cards, etc.) and lack transparency regarding interchange or network fees.

For very large volumes negotiated on a case-by-case basis, the banking model remains viable. For all others, its inflexibility ends up being costly.

The fintech model: simplicity and flexibility

In response to this system, fintech companies have turned the tables. No mandatory lease, little or no commitment, setup in just a few days, and a single, transparent rate.

But "fintech" doesn't mean much on its own. Business models vary greatly from one provider to another, especially when it comes to two factors that carry significant weight in the final calculation: the fee charged for card transactions outside Europe and the type of contract for the terminal (purchase, lease, or free with a commitment).

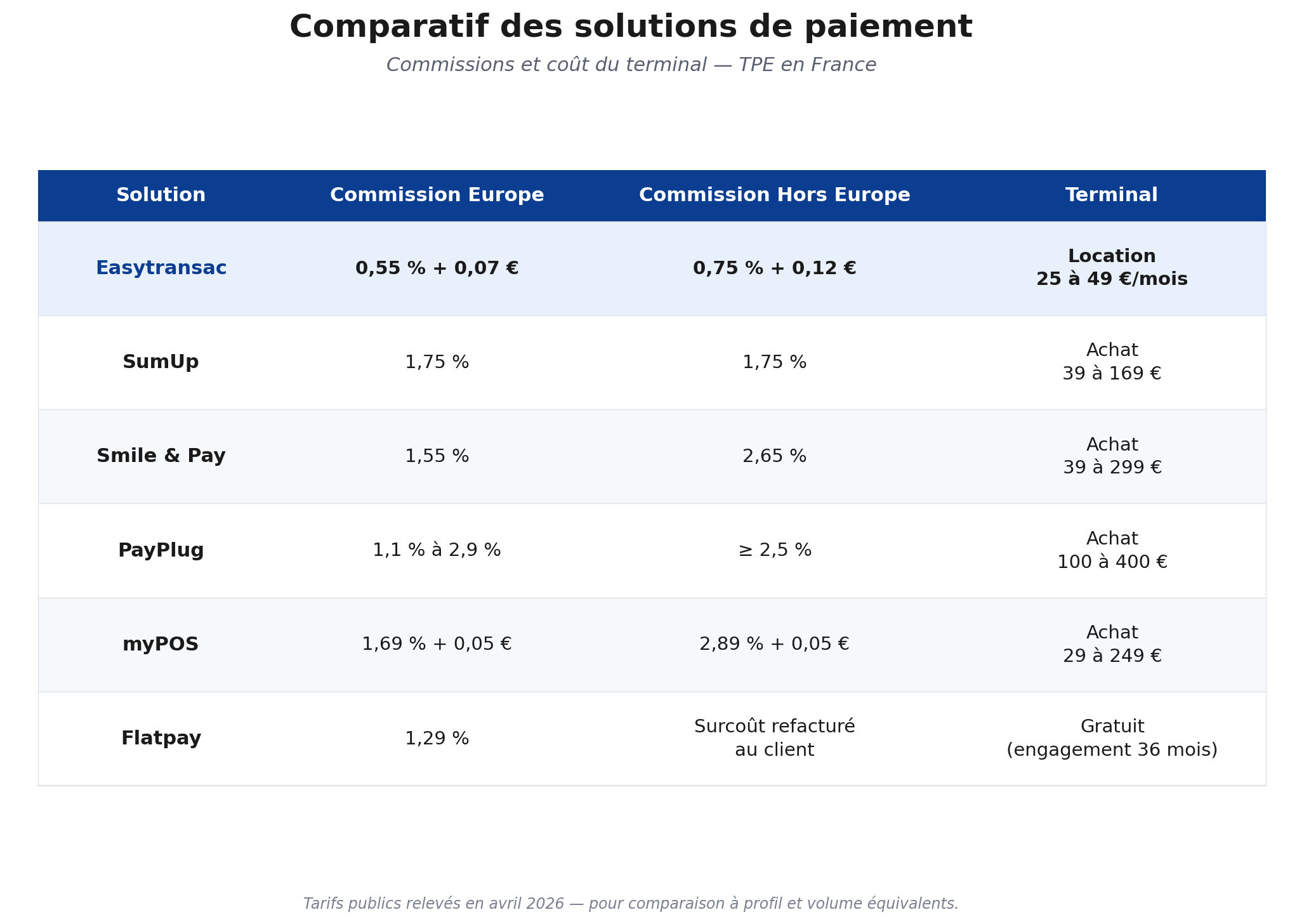

Comparison of the leading solutions

Rather than just taking the marketing hype at face value, here’s what each solution actually costs you.

SumUp

Simple model, flat rate: 1.75% per transaction, regardless of card type or issuing region. The terminalcosts between €39 (Air) and €169 (model with printer). No commitment, no mandatory subscription.

For those just starting out, this is reassuring. But as soon as monthly sales exceed a few thousand euros, that 1.75% becomes the main cost. A "Payments Plus" option for €19/month reduces the rate to 0.89% on standard cards, but remains at 1.75% on premium cards and for transactions outside the EEA.

Smile & Pay

A French provider offering an all-inclusive rate of 1.55% on European cards under the Standard plan. The payment terminal is sold separately, ranging from €39 (Mini Smile) to €299 (Super Smile). A straightforward solution with no commitment, but with a minimum fee of €4.90 (excl. tax) per month if your monthly revenue is less than €350. For cards used outside Europe, the commission rises to 2.65%, which can quickly add up in tourist areas or for international e-commerce.

PayPlug

With a stronger focus on e-commerce and omnichannel retail, PayPlug charges a wide range of fees: from 1.1% to 2.9%, depending on the plan, the type of card, and the fixed fee per transaction. Cards from outside Europe are charged a minimum of 2.5%, often more. The payment terminal costs between €100 and €400. An attractive solution for merchants already operating in e-commerce, but less straightforward for a merchant operating entirely in-store.

myPOS

Flat rate: 1.69% + €0.05 for EEA and UK cards, 2.89% + €0.05 for business cards or cards outside Europe. The terminalcosts between €29 (Go 2) and €249 (Pro), with no subscription fee. The rate seems competitive, but the fixed fee of €0.05 per transaction weighs heavily on low average order values: on a €5 purchase, that’s already 1% on top of the variable rate.

Flatpay

Aggressive pricing model at the point-of-sale terminal: free terminal. The commission is a flat rate of 1.29% on all European transactions, which is attractive. But there are two important caveats: a 36-month commitment with a penalty of €50 (excl. tax) per month if you process less than €1,300, and, more importantly, for cards from outside the EEA, the additional cost is passed directly on to the end customer —for a €100 purchase, your customer may pay €103. This is legal but can negatively impact the shopping experience, particularly in tourism or the events industry.

Easytransac

Cost-effective approach: 0.55% + €0.07 for European cards, 0.75% + €0.12 for cards outside the EEA. The POS terminal can be rented for €25 to €49 per month depending on the plan (with or without a contract), which includes technical support, updates, and hardware replacement. Easytransac also supports remote payments (payment links), e-commerce, SoftPOS (smartphone payments without a physical terminal), and Apple Pay/Google Pay wallets.

Summary table

Cards outside Europe: the hidden cost that no one notices

This is the blind spot in most comparisons. The fees listed apply to cards issued within the European Economic Area (EEA). As soon as a card is issued outside the EEA—whether for an American tourist, an Asian customer, or international online sales—the fees skyrocket.

In practical terms: for a transaction of €500 made with a U.S. credit card,

- Smile & Pay charges €7.75 (1.55%)

- myPOS charges €14.50 (2.89% + €0.05)

- PayPlug, depending on the plan, can cost €14 or more

- Easytransac charges €3.87 (0.75% + €0.12)

- Flatpay adds a surcharge that is visible to the end customer (free for the merchant)—this option is, of course, up to the merchant—who may choose to absorb these costs.

The difference is huge. For a retailer in a tourist area, a restaurant owner, a hotelier, a seasonal rental business, or an e-commerce exporter, this is often where true profitability is determined.

What really matters: the total cost over time

The classic mistake: choosing a point-of-sale system based on its purchase price. That’s a secondary consideration. Three factors really matter:

- The commission structure (variable rate, fixed portion, distinction between Europe and non-Europe) determines what you pay on each transaction.

- The monthly volume determines how much these commissions impact your P&L.

- The length of use determines whether a one-time purchase is more cost-effective than a lease that includes after-sales service and renewal.

For example: A merchant who processes €30,000 per month over four years will pay approximately €22,000 in fees with SumUp (1.75%), compared to €8,000 with Easytransac (0.55% + €0.07). The savings on fees alone far outweigh any difference in the price of the terminal.

Which solution is right for you?

For occasional or one-off sales (garage sales, pop-up markets, freelancers who rarely receive payments), a no-commitment payment solution like SumUp is sufficient. Simplicity takes precedence over profitability.

For a business that’s growing steadily, the math changes. Once you’re bringing in a few thousand euros a month, fees become the biggest expense, and a model optimized for the long term—like Easytransac — automatically becomes more cost-effective.

For businesses with an international customer base (tourism, restaurants, hotels, events, and export e-commerce), the ability to accept cards from outside Europe is a decisive factor. The cost differences between payment solutions can amount to thousands of euros per year.

Conclusion

Whether it's a bank or a fintech company, this dichotomy is actually outdated. What matters is choosing a solution that fits your business, remains transparent over time, and doesn't hide its hidden costs behind promotional rates.

Banks offer a reassuring but rigid framework. Fintech companies have become more flexible, but not all are created equal—especially when you look beyond the advertised rates. When it comes to fees within Europe, fees outside Europe, and the total cost over time, certain solutions clearly stand out for their cost-effectiveness.

Want to see how much your business would actually pay? Compare your current payment terminal with Easytransac’s rates and estimate your savings in just a few minutes.

Sources: